This article is part of the Biblically-Informed Framework for Retirement Stewardship (BIFRS) series. It was originally published on September 20, 2023, and updated in April 2026.

When I wrote this article in 2023 and interesting thing was happening: interest rates were rising for the first time since the pandemic. They were already low, and had been since 2009; in fact, they were near zero for almost five years. Rates are still higher than they were, but they have been coming back down since mid-2024. So, I have updated this article to be a more general discussion of interest rates and the different ways they affect retirees as rates rise or fall.

In a previous article, I touched on the risk that rising interest rates present to retirees. There are risks—the negative impacts of rising rates—, but there are also benefits, especially for savers and retirees.

But to the extent that higher rates are usually associated with inflation, the scale tips toward the negatives rather than the positives. In this article, we’ll look at both the challenges and benefits of rising interest rates, with a focus on their effects on retirees and those close to retirement.

The rate environment has changed

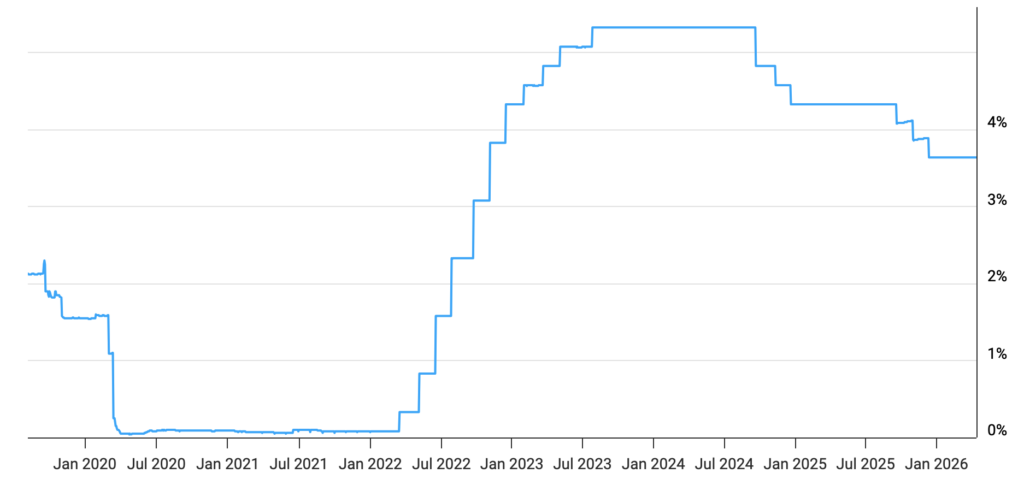

The interest rate landscape has shifted significantly since I first wrote this article in 2023. After raising rates aggressively from 2022 through mid-2024 to combat inflation, the Federal Reserve reversed course in late 2025, implementing three quarter-point rate cuts in September, October, and December. The Fed Funds rate, which peaked at 5.33% in 2023, now sits at 3.50-3.75% as of April 2026, following two consecutive meetings where the Fed held rates steady.

Fed Fund Rate: Historical Chart – 2000 to 2026

The current Fed Funds rate of 3.75% (midpoint) is down from the 5.33% peak in 2023, but still significantly higher than the near-zero rates we experienced during the 2020-2021 pandemic period. While rates have come down from their recent highs, they remain elevated compared to the decade following the 2008 financial crisis, when rates hovered near zero.

The Fed’s Balancing Act

The Federal Reserve paused rate cuts in January and March 2026 due to several factors: inflation remains above the Fed’s 2% target at around 2.7-3.3%, the job market has shown resilience despite slower hiring, and geopolitical tensions (particularly the Middle East conflict) have created economic uncertainty with energy price volatility. Fed Chair Jerome Powell has indicated the committee expects one more rate cut in 2026 and another in 2027, though the timing remains uncertain.

When it comes to interest rates and retirees, they remain a two-edged sword. Interest rates play a critical role in people’s finances in all life stages, but they can help and hurt retirees in specific ways.

This article will explore the multifaceted relationship between interest rates and retiree finances in the current environment.

The benefits

Increased Income from fixed-income investments

Most retirees have fixed-income investments, ranging from savings or money market accounts to certificates of deposits (CDs) to bonds (or bond funds). We hold these investments to diversify our portfolios, but more importantly, to generate interest that we can use as income in retirement.

While rates have come down from their 2023-2024 peaks, the news remains relatively good: Higher interest rates still mean increased returns on these fixed-income investments compared to the 2020-2021 period.

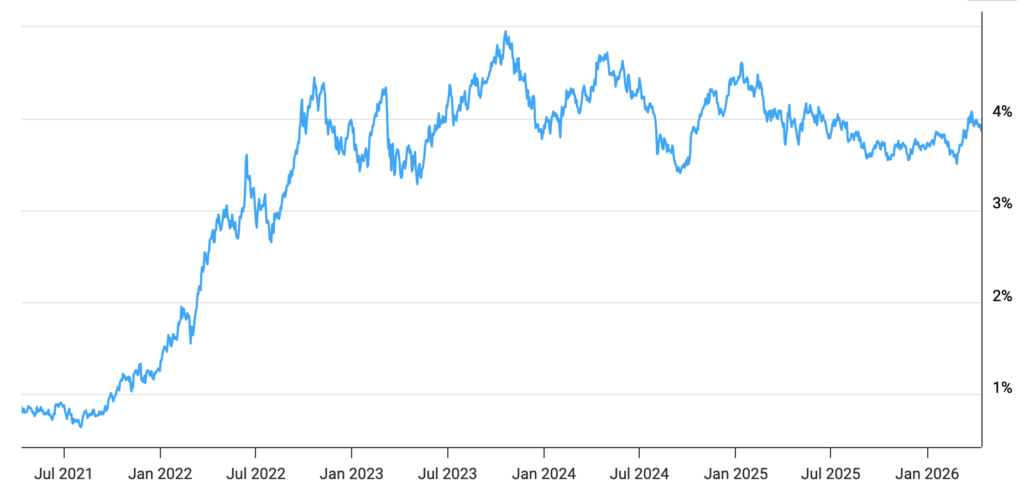

5-Year Treasuries: Current Yield – April 2026

2026 Update: Treasury yields have adjusted with the Fed’s rate cuts but remain attractive:

- 5-year Treasury notes: Currently yielding around 4.0-4.2%

- 10-year Treasury notes: Around 4.30-4.35%

- 30-year Treasury bonds: Approximately 4.50-4.60%

These yields represent a decline from the 2023 peaks (when 5-year Treasuries hit 4.5%+) but are still meaningfully higher than the sub-2% yields we saw in 2020-2021. We’re also experiencing an unusual “inverted yield curve” environment in which longer-term bonds pay slightly less than shorter-term securities, which typically signals economic uncertainty.

Corporate bonds have also adjusted. The iShares US Corporate Bond Index ETF (AGG), with an average duration of 6-7 years, is currently yielding around 4.5-5.0%.

Money market funds have come down from their peaks but still offer attractive rates. My default cash account in my Fidelity IRA is Fidelity Government Cash Reserves (FDRXX), which currently earns 3.38% (down from 4.95% in 2023, but still far better than the near-zero rates of 2020). Other popular money market funds, such as Vanguard Federal Money Market Fund (VMFXX), yield around 3.6%, and Vanguard Treasury Money Market Fund (VUSXX) pays about 3.7%.

The decline in rates has prompted me to reconsider bond strategies. Back in 2023, I had contemplated building a bond ladder and a TIPS ladder but decided against it. With rates somewhat lower but still reasonable, and given the Fed’s signal that further cuts may be coming, this might actually be a decent time to lock in some of these yields with a bond ladder or TIPS ladder. (You can read the series of articles I wrote about that HERE.)

This is still good news for retirees relying on fixed-income investments for income, though the trend is moving in the wrong direction. The key question is whether the Fed will continue cutting (which would push these yields even lower) or hold steady (or even raise rates again if inflation comes back with a vengeance)

Increased income annuity payouts

Obviously, this doesn’t affect all retirees, but conventional wisdom suggests that certain annuities may offer higher payouts when interest rates rise—and those elevated payouts have largely persisted even as rates have fallen slightly.

Insurance companies typically invest the principal they receive from customers in long-term bonds. The strong bond yields of 2022-2024 have resulted in excellent annuity payout rates that have largely remained attractive into 2026.

I ran current numbers on immediateannuities.com for my wife and me for a simple lifetime income annuity with a principal amount of $300,000 and no annual increases (meaning no adjustments to keep up with inflation), with payouts starting immediately.

At our current ages (I’m 73 and my wife is 72), our monthly income would be approximately $2,050-2,100, which represents a payout of about 8.2-8.4% annually. This is dramatically higher than any high-quality treasury or corporate bond—the 30-year treasury currently yields around 4.50%. However, keep in mind that payouts don’t mean the same thing. Annuity payouts effectively include a return of principal, whereas treasury yields are pure interest.

When I originally wrote this article in 2023, the payout was 7.16%. The improvement to 8.2-8.4% reflects both the higher interest rate environment we experienced through 2024 and the fact that we’re now three years older (age is a major factor in annuity payouts). Even with the Fed’s rate cuts in late 2025, annuity companies have largely maintained these attractive payout rates because they’re still investing in longer-term bonds that were purchased when rates were higher.

Here’s what the immediateannuities.com data shows:

Single Premium Income Annuities (SPIAs) are now near their highest levels in over a decade. A $300,000 premium would have generated an income of around 5.8% for a 70-year-old male in 2021, but today at age 73 it would pay approximately 8.2%, an increase of over 40%.

The sweet spot: We’re currently in what many financial professionals consider the “sweet spot” for annuity purchases—payouts are at decade highs, and while they may moderate slightly if the Fed continues cutting rates, they’re unlikely to decline rapidly given the lag time in how insurance companies invest premiums.

Does this mean we should all go purchase a fixed or deferred income annuity with some of our retirement savings? Not necessarily. But if you’ve been seriously considering it, this remains a favorable time to pull the trigger. I’ve written extensively about my own deliberations on this topic in my recent articles: Why Am I Reluctant to Purchase a Lifetime Income Annuity? and I’m Not as Reluctant Toward Annuities, where I analyze the hybrid strategy of combining annuities with an investment portfolio. I still think about it, but have yet to pull the trigger. If I do, I’ll let you know why I decided to.

The challenges

Bond fund volatility and the rate environment

As I shared in 2023, it was hard to see losses in our supposedly less-risky assets, like bonds, during the 2022-2023 rate increases. The Fed’s rate cuts in late 2025 provided some relief—bond prices rose as yields fell—but the overall bond market remains below its pre-2022 highs.

The iShares Core US Aggregate Bond ETF (AGG) has recovered somewhat but still shows modest losses over a 3-5 year period. Many retirees who held bond funds through the 2022-2024 period are still underwater on those positions.

The ongoing challenge is that while the Fed paused rate increases and even cut rates, uncertainty remains. If inflation re-surges (perhaps due to energy prices from Middle East tensions), the Fed could reverse course. Additionally, with the Fed signaling only gradual cuts ahead, bond investors face a period of continued uncertainty.

When bond prices fall as interest rates rise, newer bondholders benefit while long-term bondholders experience losses “on paper.” Only retirees who sell individual bonds before maturity or bond funds before interest rates stabilize and values rise will experience actual losses.

Some retirees have moved substantial portions of their savings to money market accounts earning 3.4-3.7%. While this provided safety during the volatile 2022-2024 period, there’s now a risk: as the Fed continues to cut rates, these money market yields will decline further, potentially falling back toward 2-3% or lower if we return to a more “normal” rate environment. Meanwhile, inflation—while slowing—remains above 2%, meaning real (after inflation) returns on cash could turn negative again.

Mortgage rates remain elevated

According to one source, a large majority of older households—76.2 percent of households aged 50 and over and 78.7 percent of households aged 65 and over—own their homes.

The survey also found that 44 percent of Americans aged 60 to 70 have a mortgage when they retire, and 17 percent say they may never pay it off.

During 2025 and into 2026, mortgage rates have declined from their 2023-2024 peaks but remain significantly elevated compared to the pandemic era:

- 30-year fixed mortgage: Currently averaging 6.25-6.40% (down from peaks above 7.5% in 2023, but still more than double the 3% rates of 2021)

- 15-year fixed mortgage: Around 5.60-5.75%

Rising mortgage rates remain a minimal concern for retirees who own their homes outright or who hold an ultra-low fixed-rate mortgage from 2020 to 2021. (Managing that mortgage payment in retirement is another matter, but at least the super-low rate is locked in.)

However, elevated rates continue to concern retirees who, like many others, would like to sell and purchase another house—perhaps to downsize or buy that long-awaited retirement home. If they need a mortgage, they will pay much more than they would have in 2020-2021.

Borrowing Power Comparison – 2026 vs. 2021

| Mortgage Rate | $2,000 Monthly Payment | Loan Amount | Difference |

|---|---|---|---|

| 3.0% (2021) | $2,000 | $475,000 | Baseline |

| 6.3% (2026) | $2,000 | $320,000 | -33% |

A home buyer who could afford a $2,000 monthly mortgage payment when rates were at 3.0% could borrow $475k. But with rates at 6.3%, they can only afford to borrow $320k, a 33% reduction.

Higher rates have a hidden effect: although mortgage rates have come down from their 2023 peaks, they’re still creating a “lock-in effect.” Homeowners with 3% mortgages are reluctant to sell and buy another home if it means taking on a 6%+ mortgage, which has reduced housing inventory and kept prices elevated in many markets.

Housing costs remain high despite rate adjustments

A variety of factors continue to drive house valuations higher. The conventional wisdom that higher interest rates should result in lower prices hasn’t fully materialized.

Higher rates continue to impact housing prices indirectly, and complex market dynamics remain at play:

Higher rates make housing less affordable, which means fewer people are willing to sell their current home and give up their ultra-low-interest mortgage from 2020-2021. This translates into persistently low inventory and, therefore, higher costs in areas where demand remains relatively high.

You might assume that the current housing market presents an ideal opportunity for cash buyers (many of whom are retirees) who don’t require a mortgage. However, this assumption doesn’t always hold true.

Many homeowners must sell their current home to purchase a new property. If they currently hold a 30-year mortgage locked in at 2.8-3.5% from 2020-2021, they’re unlikely to want to swap that for a potentially larger mortgage with rates around 6.3%.

So far in 2026, home prices have varied by region. Some areas saw modest declines in 2023-2024, but the national median home price has remained relatively stable or even increased in many markets. The inventory of available homes remains constrained, and this scarcity, coupled with steady (if not robust) demand, continues to support elevated prices.

The ongoing “wait-and-see” approach among potential sellers and buyers has created pent-up demand that could push prices higher if rates decline further, or lead to more significant corrections if rates rise again or economic conditions deteriorate.

Higher revolving credit interest rates

Any retirees with revolving credit accounts (credit cards) or adjustable-rate loans continue to face high interest costs, though there’s been some modest relief.

Credit card interest rates have declined slightly from their 2024 peaks but remain extraordinarily high:

- Average credit card APR for new offers: 22.1-23.7% (down from 24.9% peak in 2024)

- Average for existing accounts: 20.0-21.5%

- Range for new applicants: 5.75% to 36%, depending on creditworthiness

If you have a credit card balance of $5,000 at 22% APR, that’s $92 per month or over $1,100 in interest annually! Even with recent rate cuts, credit card rates remain stubbornly high because card companies have been slow to pass along the Fed’s rate reductions to consumers.

Home equity lines of credit (HELOCs), a popular credit option, have also come down but remain elevated. Average HELOC rates are now in the 6.5-8.5% range (down from 7-9% in 2023), compared to 4% just a few years ago.

If your revolving credit accounts are causing you problems (and they do for many retirees), the situation has improved marginally but remains challenging. See if there’s a way to pay them off without using your retirement savings. In lieu of that, refinancing with a lower-interest vehicle—perhaps a personal loan at 10-15%—may be worthwhile, though even these rates are elevated compared to recent history.

The new challenge: dealing with falling rates

When I originally wrote this article in September 2023, the dominant concern was whether rates would continue rising and how high they might go. Now, in April 2026, the conversation has shifted dramatically. We’re facing the opposite challenge: how to adapt as rates decline from their peaks—and potentially fall much further.

The Federal Reserve’s three rate cuts in late 2025 marked a significant policy reversal, and while it has paused since January 2026, the committee has signaled that further cuts are likely. For retirees, this presents a different set of challenges than we faced during the rising rate environment of 2022-2024.

The income squeeze ahead

For retirees who have come to rely on the attractive yields from money market funds and short-term bonds, falling rates represent a direct hit to income. My Fidelity Government Cash Reserves (FDRXX) that yielded 4.95% in 2023 now pays just 3.38%—a decline of more than 30%. If the Fed implements the additional rate cuts that many economists anticipate, these yields could fall to 2-3% or even lower over the next year or two.

This creates a real dilemma: Do you accept lower and lower yields on your cash, or do you extend duration (invest in longer-term bonds) to try to lock in current rates before they fall further? Each strategy carries risks. Staying in cash means watching your income decline month by month. Moving to longer-term bonds means taking on interest rate risk—if rates unexpectedly rise again, those bonds will lose value.

The CDs and bond ladder opportunity—and its closing window

There’s a potential silver lining to the current environment: we may be in a brief “sweet spot” for locking in yields. If the Fed continues cutting rates over the next 12-18 months, today’s rates on longer-term CDs (currently 4-5% for 3-5 year terms) and intermediate bonds (4-4.5%) may look attractive in hindsight.

This is why I’ve reconsidered my earlier decision not to build a bond or TIPS ladder. In 2023, I thought rates might go even higher, so I waited. Now, with the Fed clearly in a rate-cutting cycle, waiting may mean missing the opportunity to lock in these yields before they disappear. A bond ladder constructed now—with maturities spread over 5-10 years—could provide a predictable income stream even as money market rates continue to fall.

The same logic applies to CDs. A 5-year CD at 4.5% might not seem impressive compared to the 5%+ we could get in 2024, but it will look quite good if money market funds are yielding 2% in 2027.

Annuities: act now or wait?

The excellent annuity payout rates we’re seeing now—8.2-8.4% for a couple in their early 70s—are largely a function of the higher-interest-rate environment of 2022-2024. Insurance companies invest premiums in long-term bonds, so today’s payout rates still reflect the higher yields available when many of those bonds were purchased.

However, as rates continue to fall and insurance companies invest new premiums in lower-yielding bonds, annuity payout rates will inevitably decline. The question is: how quickly? There’s typically a lag of 6-18 months before falling interest rates fully work their way into annuity pricing.

For retirees contemplating an annuity purchase, this creates urgency. The window for locking in these historically attractive payout rates may be closing. Waiting to see if rates fall further risks annuity payouts declining faster than Treasury yields, potentially leaving you with a worse deal overall.

The bond fund opportunity

One benefit of falling rates is that bond funds—which suffered losses during the 2022-2024 rate increases—should see capital appreciation as rates decline. Bond prices move inversely to yields: when yields fall, bond prices rise.

For retirees who held bond funds through the painful 2022-2024 period and are still sitting on losses, there’s a recovery opportunity ahead. The iShares Core US Aggregate Bond ETF (AGG) and similar funds should see price increases if the Fed follows through with additional cuts. This doesn’t help generate income, but it does help restore portfolio values that were damaged during the period of rising rates.

Of course, this assumes rates do continue to fall. If inflation resurges or geopolitical events force the Fed to reverse course again, bond funds could experience renewed losses. This is why many financial advisors suggest holding bonds to maturity (via individual bonds or a bond ladder) rather than relying on bond funds if you need the income and can’t tolerate volatility.

Adjusting your strategy for a falling rate environment

The shift from rising rates to falling rates requires retirees to reconsider their strategies:

If you’re heavily in cash or short-term bonds, consider extending duration now to lock in current yields before they fall further. A laddered approach—with maturities spread across 2-10 years—can provide both liquidity and higher yields than money market funds.

If you’re considering an annuity, the current environment may favor acting sooner rather than later. Payout rates are still near decade-highs, but they’re unlikely to remain this attractive if rates continue to fall.

If you hold bond funds with losses, consider holding on through the recovery, assuming the fund’s bonds align with your time horizon and risk tolerance. Price appreciation from falling rates should help recoup some of those losses.

If you have adjustable-rate debt: The good news is that HELOCs and other adjustable-rate loans should see their rates decline as the Fed continues to cut rates. Credit card rates, unfortunately, tend to be stickier on the way down than they were quick to rise.

The key is recognizing that the interest rate environment is dynamic. The strategies that worked in the rising rate environment of 2022-2024 may not be optimal now that rates are falling. Flexibility and periodic reassessment of your approach will be essential.

Take the good, deal with the bad

Interest rates remain a double-edged sword for retirees, offering benefits and challenges—though the blade is somewhat less sharp than it was in 2023. While rates have come down from their peaks, they’re still elevated compared to the decade preceding 2022. The current environment offers moderately attractive income opportunities for fixed-income investments and excellent annuity payout rates, but challenges persist, including bond fund volatility, elevated mortgage rates, high housing costs, and stubbornly high credit card interest rates.

Looking ahead: The Federal Reserve’s path forward remains uncertain. While they’ve signaled potential for additional cuts in 2026 and 2027, geopolitical tensions, inflation concerns, and economic data will drive their decisions. For retirees, this means continued uncertainty but also potential opportunities:

- If rates continue to fall, money market and bond yields will decline further, but bond fund values should rise, and mortgage rates should improve

- If rates hold steady or rise: Cash and short-term bonds will maintain current yields, but bond funds could face renewed pressure, and the housing market may see more significant corrections

An excellent way to navigate this complex and evolving relationship between interest rates and retirement—both the benefits and challenges—is to maintain a diversified portfolio, regularly review your financial plans, watch your spending, and consult with your financial advisor if you have one, who can help you develop a personal strategy to deal with these changing economic conditions.

Navigating these choppy economic waters requires wisdom and faith. If you’re tempted toward anxiety or fear of what the future holds, remember this: The Bible describes faith as the assurance of something we hope for that we do not presently have (Heb. 11:1). God is sovereign over all, including the U.S. economy, and these challenges can help us cultivate wisdom and develop our faith in Him.

So, putting your faith and trust in God and being flexible and adaptable with your financial plans can help you find peace as you stay the course, regardless of the interest-rate environment.

As a retiree now fully navigating these conditions, I can testify that the moderate income from cash reserves and bonds, along with stock dividends, has made this rate environment more favorable for retirees than the near-zero rate period of 2020-2021. While volatility and uncertainty remain, maintaining a balanced approach—with appropriate allocations to cash, bonds, stocks, and potentially annuities—continues to be the best strategy for weathering whatever rate environment lies ahead.