This article is part of the Biblically-Informed Framework for Retirement Stewardship (BIFRS) series. It was originally published on September 5, 2016, and updated in April 2026.

When I first wrote this article in 2016, my wife and I were closing in on Medicare eligibility at age 65. We were trying to navigate the complexity from the outside, making educated guesses about what we’d choose.

Now, in 2026, we’ve been on Medicare for more than nine years. We’ve lived through the enrollment process, made our plan choices, experienced the costs and coverage firsthand, and navigated the annual review process every fall.

The good news is that the framework I laid out in 2016 was solid. The decisions we made were the right ones for us. The bad news: Medicare has only gotten more complex, with more plan options, higher costs, and more income-based surcharges than when I first wrote this.

My wife and I both navigated Medicare eligibility starting at age 65. In this article, I’ll share what we learned—both from the initial research and from nearly a decade of experience living with these decisions.

Our situation was similar to many others’. We were initially covered by an employer health plan, but we knew that, once we retired, it would no longer be the case. I was still working when my wife became eligible for Medicare, which added complexity to our decisions.

Medicare Explained

Here’s how it works: The US Government subsidizes medical insurance for certain disabled individuals and everyone who has reached 65 years of age. (This generally applies only to citizens and legal immigrants.) Medicare has “Parts”—not numbered one through four, but identified as Part A, Part B, Part C, and Part D. In addition, the coverage for each Part has deductibles and upper limits. Deductibles can be reduced and limits increased with Medicare Supplemental Insurance (usually called Medigap insurance).

In general, the four Parts and Medigap programs are as follows:

Part A: Hospital Charges

This covers hospital charges, but not your doctor’s fees or medications. It has a deductible and coverage limits (as most medical insurance does). Currently, you can receive this coverage without additional charge if you (or your spouse) have paid into Social Security for at least 40 quarters (10 years of work). Having this coverage generally limits your exposure to catastrophic hospital charges.

2026 Part A Costs (Official CMS Data):

- Most people: $0 monthly premium (if you or your spouse has 40+ quarters of coverage)

- 30-39 quarters: $311/month premium

- Fewer than 30 quarters: $565/month premium

- Inpatient hospital deductible: $1,736 per benefit period (up from $1,676 in 2025)

- Days 61-90: $434/day coinsurance

- Lifetime reserve days (91-150): $868/day coinsurance

It is critically important to note that Part A does not cover long-term care expenses. Separate, private insurance is needed for that.

Part B: Medical Insurance

This pays for doctors’ bills, outpatient care, preventive services, and durable medical equipment. It also has a deductible and coverage limits. This Part is optional, and you will be charged monthly for this coverage.

2026 Part B Costs:

- Standard monthly premium: $202.90 (up from $185.00 in 2025—a 9.7% increase)

- Annual deductible: $283 (up from $257 in 2025)

- Coinsurance: Typically 20% of Medicare-approved amounts after deductible

- The Federal Government pays approximately 75% of Part B costs; individuals pay 25% through monthly premiums

Nearly everyone covered by Part A also chooses to be covered by Part B. You may delay signing up for Part B if you have other creditable insurance (such as an employer plan with 20+ employees) without incurring a late-enrollment penalty.

Late Enrollment Penalty: If you delay enrolling in Part B without creditable coverage, you’ll be penalized at the rate of 10% for each 12-month period of delay. This penalty is permanent and compounds over time. Don’t miss your enrollment windows.

Our Part B premium increased for 2026. It was the second-highest dollar increase in Medicare history ($17.90/month). Combined with a modest 2.8% Social Security COLA ($56/month average increase), Medicare premiums consumed nearly one-third of the Social Security increase for many retirees. This is why I recommend building Medicare cost increases into retirement budgets at 5-7% annually rather than general inflation rates.

Part B income-related monthly adjustment amount (IRMAA)

This doesn’t apply to most retirees, but higher-income beneficiaries pay surcharges on top of the standard Part B premium through IRMAA. These surcharges are based on your Modified Adjusted Gross Income (MAGI) from two years prior—your 2026 premium is based on your 2024 tax return.

2026 IRMAA Brackets (Official SSA Data):

| Individual MAGI | Joint MAGI | Monthly Part B Premium | IRMAA Surcharge |

|---|---|---|---|

| ≤$109,000 | ≤$218,000 | $202.90 | $0 |

| $109,001-$137,000 | $218,001-$274,000 | $284.10 | $81.20 |

| $137,001-$172,000 | $274,001-$344,000 | $405.30 | $202.40 |

| $172,001-$205,000 | $344,001-$410,000 | $526.50 | $323.60 |

| $205,001-$500,000 | $410,001-$750,000 | $647.70 | $444.80 |

| >$500,000 | >$750,000 | $689.90 | $487.00 |

This is a cliff, not a bracket. Going from $218,000 to $218,001 in MAGI costs a married couple an extra $1,948.80 annually ($81.20 × 2 × 12 months). This makes strategic income planning essential.

Part C: “Medicare Advantage” plans

These are comprehensive plans offered by private insurance companies that combine Part A and Part B coverage (and usually Part D prescription drug coverage). They typically operate like HMOs or PPOs with provider networks, but often include additional benefits like dental, vision, hearing, and fitness programs that Original Medicare doesn’t cover.

Key Trade-offs:

- Lower monthly premiums (many plans have a $0 premium beyond Part B)

- Additional benefits (dental, vision, hearing)

- But: Network restrictions, prior authorization requirements, and annual out-of-pocket maximums ($9,250 max in 2026)

Far more people are enrolled in Original Medicare (Parts A and B) plus Medigap than in Medicare Advantage, though Advantage enrollment has grown significantly in recent years.

The decision between Original Medicare plus Medigap vs. Medicare Advantage is one of the most important Medicare decisions you’ll make. (See the decision framework section below.)

Part D: prescription drug coverage

Part D covers prescription medications and is provided by private insurance companies approved by Medicare. Coverage and costs vary significantly by plan, geographic region, and which medications you take.

2026 Part D Information (Medicare.gov):

- Average monthly premium: $34.50 (down from $38.31 in 2025, thanks to federal premium stabilization programs)

- Maximum deductible: $615 (plans can have lower or $0 deductibles)

- Coverage gap (“donut hole”): Eliminated as of 2025 (no longer applies)

- Catastrophic coverage threshold: $8,000 in out-of-pocket costs

- Insulin copay cap: $35/month maximum for covered insulin products

Important: There is a late-enrollment penalty for Part D (1% of the national base beneficiary premium for each month of delay). This penalty is permanent and compounds annually.

Part D IRMAA Surcharges (2026):

The same IRMAA income brackets that apply to Part B also apply to Part D, with additional monthly surcharges:

| Individual/Joint MAGI | Part D IRMAA Surcharge |

|---|---|

| ≤$109K / ≤$218K | $0 |

| $109K-$137K / $218K-$274K | $14.50 |

| $137K-$172K / $274K-$344K | $37.30 |

| $172K-$205K / $344K-$410K | $60.10 |

| $205K-$500K / $410K-$750K | $82.90 |

| >$500K / >$750K | $91.00 |

Annual Review is Essential: During the Annual Enrollment Period (October 15-December 7), you can use Medicare’s Plan Finder tool to compare Part D plans based on your actual prescriptions. Plans change their formularies, pricing tiers, and pharmacy networks annually. What was the best plan last year may not be this year.

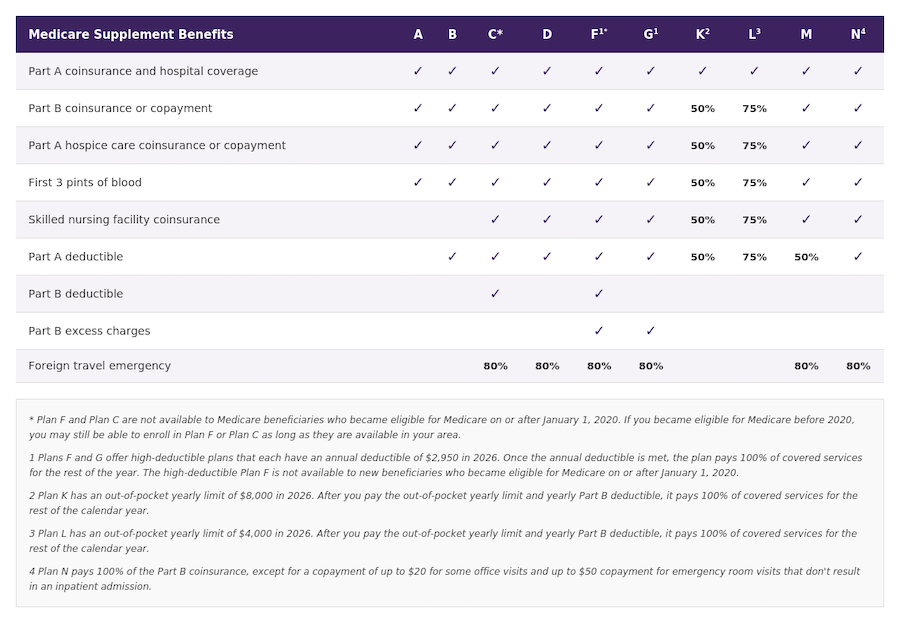

“Medigap” insurance (Medicare supplement)

Medigap is a predefined set of standardized plans (Plans A through N), specified by the federal government and offered by private insurance companies. These plans fill in the “gaps” left by Original Medicare—deductibles, coinsurance, and copayments.

The Most Popular Medigap Plans in 2026:

Plan G (most popular for new enrollees):

- Covers: Part A deductible, Part A coinsurance, Part B coinsurance (20%), first 3 pints of blood, Part A hospice coinsurance, skilled nursing coinsurance, Part B excess charges, foreign travel emergency care

- Does NOT cover: Part B deductible ($283 in 2026—you pay this once annually)

Plan F (no longer available to new enrollees):

- Most comprehensive coverage

- Only available if you became Medicare-eligible before January 1, 2020

- Covers everything Plan G covers, PLUS the Part B deductible

Plan N (growing in popularity):

- Similar to Plan G but with small copays ($20 office visit, $50 ER visit)

- Lower premiums than Plan G

Medigap Pricing:

Medigap premiums vary significantly by state, zip code, age, gender, tobacco use, and pricing method. Insurance companies use three pricing methods:

- Community-rated: Same premium regardless of age

- Issue-age-rated: Premium based on age when you enroll; doesn’t increase with age

- Attained-age-rated: Premium increases as you age (most common)

Typical 2026 Plan G Monthly Premiums (Attained-Age):

- Age 65: $125-$180

- Age 70: $150-$200

- Age 75: $175-$230

- Age 80: $195-$260

(Rates vary dramatically by location. Some states are 30-40% higher or lower than these national averages.)

My wife and I have Plan F (grandfathered in before 2020). Our premiums have increased about 4-6% annually, which is typical for Medigap. But the coverage has been excellent—we never worry about surprise medical bills or hitting spending limits. For us, the predictability and comprehensive coverage are worth the monthly premium.

Decisions, decisions

Everyone approaching Medicare will need to make several critical decisions:

Decision #1: Original Medicare + Medigap OR Medicare Advantage?

This is the fundamental choice. Here’s a framework:

Choose Original Medicare + Medigap if you:

- Want complete freedom to see any doctor accepting Medicare nationwide

- Travel frequently or split time between multiple locations

- Have complex health conditions requiring multiple specialists

- Value predictable costs and minimal paperwork

- Can afford higher monthly premiums for comprehensive coverage

Choose Medicare Advantage if you:

- Want lower monthly premiums (possibly $0 beyond Part B)

- Don’t travel much and are comfortable with network restrictions

- Want dental, vision, hearing, and fitness benefits included

- Are healthy and expect routine care needs

- Can manage prior authorization requirements

There is no universally “right” choice. We chose Original Medicare + Plan F because we value flexibility and predictability. Friends who rarely see specialists and don’t travel much love their $0-premium Advantage plans.

Decision #2: Which Part D plan?

Use Medicare.gov’s Plan Finder tool. Enter your actual prescriptions, your preferred pharmacies, and your zip code. The tool ranks plans by total annual cost (premiums + your drug costs).

Don’t just pick the lowest premium—look at total annual cost including copays. A plan with a $0 premium might cost you $2,000 in drug copays, while a $50/month premium plan might cost you $600/year in drug copays plus $600 in premiums ($1,200 total).

Decision #3: Which Medigap Plan (if choosing Original Medicare)?

As you can see in the chart below, for most new enrollees, Plan G offers the best value. It’s nearly as comprehensive as Plan F (which is not available to retirees who became eligible for Medicare on or after January 1, 2020), but costs less because you pay the $283 annual Part B deductible yourself. This is a reasonable trade-off for most people.

Shop multiple insurance companies. Medigap plans are standardized—Plan G from Company A provides identical coverage to Plan G from Company B. But premiums can vary by 30-50% or more. Get quotes from at least 3-5 companies.

Enroll during your Medigap Open Enrollment Period (6 months after enrolling in Part B). During this period, you have guaranteed issue rights—no medical underwriting, no questions about health conditions, no denials. If you wait and develop health issues, you may be denied Medigap coverage entirely or charged much higher rates.

Important enrollment periods

Initial Enrollment Period (IEP): 7 months total—3 months before your 65th birthday month, your birthday month, and 3 months after.

General Enrollment Period: January 1-March 31 each year (if you missed your IEP). Coverage starts July 1. Late penalties apply.

Special Enrollment Period (SEP): Available if you (or your spouse) have employer coverage from a company with 20+ employees and are still working. You can delay Part B enrollment without penalty while covered by current employer insurance, then enroll when that coverage ends (up to 8 months after employment/coverage ends) without penalty.

Annual Enrollment Period (AEP): October 15-December 7 each year. You can switch Part D plans or switch between Original Medicare and Medicare Advantage.

Don’t miss these windows. Late enrollment penalties for Part B and Part D are permanent and compound over time. They can cost thousands of dollars over a 20-30 year retirement.

Our “special situation” (and yours might be too)

When my wife became Medicare-eligible, I was still working, and we both had employer-sponsored health insurance from my employer. This created what Medicare calls a “special situation.”

Here’s how it works:

If you or your spouse have current employer coverage from a company with 20+ employees:

- You can delay enrolling in Part B without penalty

- You qualify for a Special Enrollment Period (SEP)

- You can enroll anytime while still employed AND up to 8 months after employment/coverage ends

- No late-enrollment penalty applies

IMPORTANT: The employer insurance must be from “current employment,” not retiree coverage, and from a company with 20+ employees. Otherwise, it doesn’t count as creditable coverage, and you’ll face late-enrollment penalties if you delay.

COBRA IS NOT CURRENT EMPLOYER INSURANCE. If you retire before 65 and use COBRA until Medicare eligibility, you must enroll in Medicare at your Initial Enrollment Period, or you’ll face penalties. COBRA doesn’t qualify for the Special Enrollment Period exception.

Here’s a helpful chart from Kiplinger.com showing how employer coverage interacts with Medicare:

| Situation | Recommendation |

|---|---|

| Working, the employer has fewer than 20 | Can delay Part B, use SEP later |

| Enroll in Part B at the IEP in most cases | Enroll in Part B at 65 (Medicare becomes primary) |

| Retired, using COBRA | Enroll in Part B at IEP (COBRA doesn’t extend SEP) |

| Spouse working, on spouse’s plan (20+ employees) | Can delay Part B, use SEP later |

| Retiree health coverage (not COBRA) | Enroll in Part B at IEP in most cases |

In our case, my employer’s plan was the primary payer, so my wife initially delayed enrolling in Part B. When I retired, and we lost employer coverage, she (and I) enrolled using our Special Enrollment Period without any penalties.

This provision provides tremendous flexibility for those still working past 65 or covered by a working spouse’s plan.

Practical action steps

If you’re 64 years, 9 months old (approaching your IEP):

- Contact Social Security by phone (1-800-772-1213) or online at SSA.gov even if you’re not ready to enroll yet. Ask about:

- Your eligibility for Part A premium-free coverage

- Whether you should delay Part B (if you have employer coverage)

- Necessary documentation and timing

- If you have employer coverage: Contact your HR department and ask:

- How many employees does the company have (is it 20+)?

- Will your coverage remain primary after you turn 65?

- Do you need to enroll in Part A, Part B, or both at 65?

- What certificates or documentation do you need?

- Research Part D plans using Medicare.gov’s Plan Finder (even if you’re delaying Part B)

- Research Medigap plans (if choosing the Original Medicare route) and get quotes from multiple insurers

- Mark your calendar: Your Medigap Open Enrollment Period begins the month your Part B coverage starts and lasts 6 months

If you’re already on Medicare:

- Review coverage annually from October 15 to December 7

- Update Medicare.gov Plan Finder with current medications

- Check if doctors are still in-network (if Medicare Advantage)

- Watch for IRMAA letters from Social Security (based on tax returns from 2 years prior)

- Consider whether your plan still fits your needs as your health status changes

The bottom line

Medicare is complex. The decisions you make at 65 will affect your healthcare costs, coverage, and peace of mind for potentially 20-30 years.

The good news: Once you understand the framework (Parts A, B, C, D; Medigap; IRMAA; enrollment periods), the decisions become manageable. And while the system is complicated, most of the complexity comes from having options—which is ultimately a good thing.

After nearly a decade on Medicare, here’s what I’ve learned:

1. The initial enrollment decisions matter enormously. Choose wisely during your Initial Enrollment Period and Medigap Open Enrollment Period. These windows give you guaranteed coverage that you may never get again.

2. Annual review is non-negotiable. Plans change, formularies change, your health changes. Spend an hour every October comparing options. It consistently pays off.

3. IRMAA planning matters more than most people realize. If your income is anywhere near the first IRMAA threshold ($109K individual / $218K joint), strategic tax planning can save thousands annually in Medicare premiums.

4. The system is navigable. Yes, it’s complex. But millions of people successfully enroll in Medicare every year. You can do this.

5. Faithful stewardship includes planning for healthcare. Proverbs 27:12 says, “The prudent see danger and take refuge, but the simple keep going and pay the penalty.” Planning for Medicare is exactly this—seeing healthcare costs ahead and preparing wisely.

As you approach Medicare eligibility, remember: This is part of the Caregiving Principle. Planning well for your own healthcare needs ensures you won’t become an unnecessary burden on your family. It positions you to receive care when needed without creating a financial crisis. And it honors the gift of life and health that God has given you.