This article is part of the Retirement Financial Life Equation (RFLE) series. It was initially published on November 11, 2020, and updated in March 2026.

This article is the second in a three-part series on the “Bucket Strategy.”

The bucket strategy is a good one, but it’s not perfect. I have been using a version of the bucket strategy since I retired in 2018, and after more than seven years of real-world experience, I still think it is a sound strategy—especially in maintaining a cash bucket for spending during falling stock markets.

In the five years since I originally wrote this article, many of the concerns I raised have been addressed by the dramatically improved interest rate environment. When I wrote this in November 2020, we were in an unprecedented ultra-low rate environment with near-zero cash yields and bonds struggling to generate 2-3% returns. That made income generation extremely challenging.

Today’s environment (December 2025) is radically different:

- Cash and money markets: 4-5% yields

- Short-term bonds: 4-5%

- Intermediate bonds: 4.5-5.5%

- Single Premium Immediate Annuities (SPIAs): 8.1% for a 73-year-old

This transformation has made the bucket strategy—and its variations—significantly more viable and effective. The core challenges I identified in 2020 remain conceptually important, but their severity has been substantially reduced by improved yields. That said, understanding these potential weaknesses helps you prepare for future low-rate environments and build appropriate safeguards into your strategy.

The best strategy is the one that is right for you and your situation. So, first, you have to get the information you need to understand your options, and also get wise advice and counsel from others as needed:

Proverbs 15:22: Without counsel plans fail, but with many advisers they succeed. (ESV)

Then, even after you choose a strategy, including any of the bucket approaches, you need to anticipate that there might be problems and prepare accordingly:

Proverbs 27:12: The prudent sees danger and hides himself, but the simple go on and suffer for it. (ESV)

The bucket strategy’s strengths appear to outweigh its weaknesses, though there are still weaknesses. We’ll look at some variations of the strategy you may want to consider.

Potential weakness #1: Low-interest rates and stock dividends

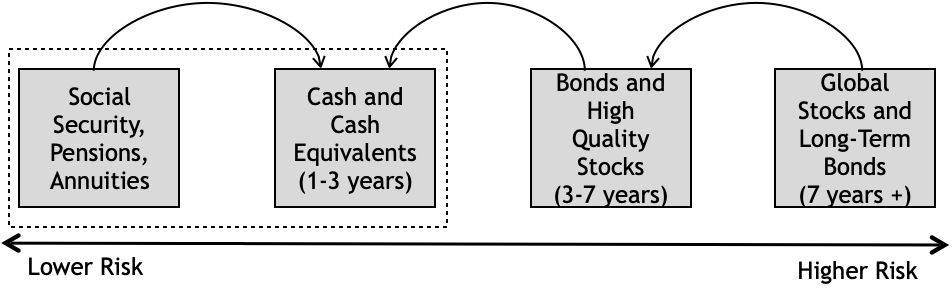

As we have seen, the bucket strategy’s primary goal (and potential benefit) is to mitigate market volatility. It can also reduce the adverse effects of a sharp, prolonged downturn at the beginning of retirement (sequence-of-returns risk) by drawing on Cash Bucket #1 rather than selling income-generating or growth assets in Bucket #2 or #3.

Most users of the bucket strategy prefer to replenish Bucket #1 with interest and dividends from Buckets #2 and #3. That leaves the assets in both buckets to grow, hopefully, at least enough to beat inflation.

As I noted in my 2020 article on low interest rates, near-zero rates resulted in minimal interest income from Bucket #2. That made it extremely challenging to keep Bucket #1 refilled unless stock dividends made up the difference.

Yet in severe recessionary periods, companies may also reduce stock dividends. Low-interest rates and reduced dividends create a “double-whammy” adverse effect on retirement income.

In a worst-case, extended-down-market scenario, you could mostly deplete Bucket #1, especially if Bucket #2 doesn’t generate enough income to refill it. You may also deplete Bucket #2 if you must sell income-producing assets to fund Bucket #1.

The improved rate environment has dramatically reduced this risk. With cash earning 4-5%, short-term bonds yielding 4-5%, and intermediate bonds at 4.5-5.5%, income generation from Buckets #1 and #2 is now realistic without excessive risk-taking. Additionally, dividend yields on quality stocks remain in the 2-3% range, providing meaningful supplemental income.

This doesn’t mean the risk has disappeared entirely—a future return to ultra-low rates could resurrect these challenges. But for now, the bucket strategy is operating in a much more favorable environment than when I wrote the original article.

That said, dividend cuts remain a concern during severe recessions. During the 2020 pandemic, some companies reduced or suspended dividends, although many high-quality dividend payers maintained them. Diversification across dividend-paying stocks and adequately funding Buckets #1 and #2 remain essential safeguards.

Potential weakness #2: Prolonged downturn

The main advantage of the bucket strategy is that it may help you hang tough and not sell depreciated assets during a down market. But what if the market doesn’t rebound in two to three years or longer?

You might have to do some severe spending “belt-tightening” if Bucket #1 is significantly depleted. During the 2008-2009 recession, many experienced this, though the market rebounded relatively quickly from the pandemic-related crash in early 2020.

Having now lived through the 2022 bear market (where stocks fell over 18% and bonds declined simultaneously—unusual and particularly challenging), I can confirm that the bucket strategy provided genuine peace of mind. Because I had adequate cash reserves, I never felt pressure to sell depreciated assets, and I was able to weather the downturn without undue anxiety.

However, this experience reinforced the importance of two things:

- Adequate bucket sizing: My 10-year “reserve” (2 years cash + 2 years short-term bonds + 6 years intermediate bonds/balanced funds) proved more than sufficient

- Income generation: The improved yields meant my buckets were generating enough income to help maintain themselves even during the downturn

In a prolonged scenario where Bucket #1 becomes significantly depleted and Bucket #2 has not kept pace, you may have to draw from Bucket #3, which has also likely declined due to the market downturn. That forces you to move assets targeted for use more than 10 years later from Bucket #3 to Bucket #1 or #2.

Before implementing this strategy, ensure you understand this potential risk. Consider this: How would you feel if you had to sell stock assets in Bucket #3 that had depreciated 30% in value to add to Bucket #1 so that you can pay your bills?

This is where the integration of the bucket strategy with variable withdrawal approaches like guardrails becomes powerful. If you’re using a guardrails approach, you would plan in advance to reduce discretionary spending by 10% if your portfolio hits certain thresholds. This reduces the pressure on all your buckets and gives them more time to recover.

For example, if you have $36,000 in Social Security and plan for $26,000 in portfolio withdrawals ($62,000 total), a 10% guardrails cut would reduce portfolio withdrawals to $23,400—only a 4.2% reduction in total income. Most retirees can adjust discretionary spending (e.g., travel, dining out, gifts) by this amount without significantly affecting their quality of life.

Potential weakness #3: Sacrificing growth for “safety”

The Bucket Strategy differs from typical strategies that focus on the optimal stock-bond allocation in a portfolio based on risk tolerance (i.e., the greatest loss a retiree believes he or she can tolerate in a market downturn). Traditional risk-based strategies are also tied to optimal asset allocation to prevent premature depletion of the savings portfolio, using safe withdrawal rates.

Many retirees may find that setting aside three years of cash in Bucket #1 and seven additional years of lower-growth assets in Bucket #2, comprises almost half of the assets in their portfolio. Such a high allocation to bonds and cash may differ from the more aggressive stocks-to-bonds allocation they maintained during the “accumulation phase” (e.g., 80/20, 70/30, 60/40 stocks-to-bonds).

Therefore, the concern is that the “safety” of maintaining a large cash balance may come at the expense of long-term growth.

Many financial planning professionals caution that being overly conservative (i.e., maintaining excessive cash and fixed-income securities in Buckets #1 and #2) can result in a less sustainable portfolio over the long term. In other words, increasing the security of your income for the next ten years in case of a long-term recession may come at the expense of less security in the ten or twenty years after.

Recent research from Morningstar and Bill Bengen provides interesting insights here:

- Bengen’s 2025 update: He now recommends 47-75% stocks (with 4.7% starting withdrawal rate) and explicitly warns that reducing stock allocation during retirement is the worst approach. Maintaining or gradually increasing equity exposure produces better outcomes.

- Morningstar’s findings: For a 3.9% fixed withdrawal rate over 30 years, optimal stock allocation is only 20-50%. However, this assumes a very conservative spending system.

- The bucket strategy sweet spot: With approximately 40% in Buckets #1-2 (cash and bonds) and 60% in Bucket #3 (growth assets with perhaps 35-40% in stocks), the bucket strategy actually aligns well with research recommendations—especially if you’re using a variable withdrawal approach.

The key insight: The bucket strategy isn’t necessarily over-conservative if your Bucket #3 is properly allocated to growth assets. A 60% allocation to growth assets (which might be 35-40% stocks, 20-25% higher-income bonds/preferreds, and 5% REITs) is reasonable for sustainable retirement income.

Delicate balancing act

The bucket strategy isn’t a no-maintenance approach; managing it is a delicate balancing act.

On the one hand, you need to withdraw cash to help cover your monthly expenses. On the other hand, you need a suitable plan to ensure that Bucket #2 generates sufficient income to fill Bucket #1 and that Bucket #3 grows to provide for future spending and at least enough to keep up with inflation.

The greatest challenge comes when a bucket fails, especially Bucket #1. Increasing the cash bucket by selling assets in Bucket #2 or #3 to avoid failure may reduce expected long-term portfolio returns. And the income for future years funded by growth stocks is put at risk.

You now see the inherent “tension” in the bucket-oriented portfolio: long-term success hinges on the performance of Buckets #2 and #3.

After seven years of managing my bucket strategy, I’ve learned that annual reviews and rebalancing are essential but not overly burdensome:

- Annual check-up (December): Review bucket balances against targets

- Rebalance opportunistically: In strong market years, take profits from Bucket #3 to rebuild #1 and #2

- Income flows naturally: With improved yields, much of the refilling happens automatically from interest and dividends

- Stay flexible: Adjust bucket sizes as needed based on changing circumstances

The strategy does require more active management than a simple total-return approach, but the psychological benefits (sleeping well during downturns) are worth the effort for many retirees.

Variations

It becomes clear that the fewer savings you have, the less likely the traditional bucket strategy is to be optimal for you. Those with lower total savings may need to keep less in Buckets #1 and #2, so they have enough in Bucket #3 (the growth bucket) to make their savings last as long as possible. The challenge lies in accepting the stock-market risk that accompanies it.

Also, in a prolonged economic slump, you may be drawing down Bucket #1 and replenishing it from Buckets #2 and #3. If those buckets are also down in value, then your overall portfolio value is declining.

If you tap Bucket #3 prematurely, you are using funds intended for ten or more years out. Premature tapping of Bucket #3 increases the risk that you will fully deplete your savings before your time on earth ends.

I must confess that when I wrote the original article in 2020, I had second thoughts about the bucket strategy due to the ultra-low interest rate environment. Five years later, with rates normalized and having successfully navigated various market conditions, including a bear market, I’m now more confident in the strategy—with appropriate modifications based on individual circumstances.

Fortunately, a couple of “modified bucket strategies” at least partially address these potential weaknesses and have become even more attractive in the current environment.

Variation #1: The bucket strategy with an income floor

The standard “bucket strategy” is not an “income floor” strategy, but most people already have a “floor” in the form of Social Security and perhaps a pension. A modified approach adds more “guaranteed income” to create a reliable lifetime income floor for essential expenses, combined with the bucket approach for discretionary spending and growth.

Bucket #1: The Income Floor

Creating this income floor could completely replace the traditional Bucket #1 since you don’t have to continually replenish it with income from other assets. Or, you could still have a smaller cash bucket and supplement it with an income floor (although it’s not technically a “bucket” since you can’t deplete it and don’t refill it regularly).

With this approach, rather than relying only on interest and dividends from Bucket #2 (and perhaps #3), you would use something like a single-premium immediate annuity (SPIA) combined with your Social Security income to cover your essential expenses.

This variation has become significantly more attractive in 2025. When I wrote the original article in 2020, SPIA payout rates for a 70-year-old were approximately 5-6%. Today, rates have soared to approximately:

- Age 73: 8.1% annual payout

- Age 70: ~7.5% annual payout

- Age 75: ~8.5% annual payout

These are the highest payout rates in over a decade and represent a transformational improvement. For context:

- On a $100,000 SPIA purchase at age 73, you’d receive $8,100 annually for life

- This nearly doubles your “income floor” compared to what was available in 2020

- The breakeven point is now much more favorable (roughly 12-13 years vs. 17-18 years)

Most people will need to fund the annuity purchase using a portion of their retirement savings. Most financial professionals suggest that you not allocate more than 25 to 35 percent to this purpose to leave yourself some flexibility in the future. Remember, you hand over a pile of money to an insurance company when you buy an immediate income annuity—though with 8.1% payouts, that trade-off is much more palatable than it was.

Important annuity considerations:

Since most immediate annuities are not inflation-protected, you want to retain some growth assets as well, primarily in Bucket #3. You can get graduated annuities that increase a certain percentage each year (typically 2-3%), but they start with significantly lower initial payouts and aren’t based on actual inflation.

For most people, committing to an annuity remains a tough decision. The idea of taking a large sum of money out of their savings is the primary inhibitor. You may be concerned about trusting an insurance company with all that money. If so, you might spread your SPIA purchases across a few high-quality (A+ rated or better) companies and stay within your state’s insurance guaranty program limits (typically $250,000-$500,000, varying by state).

You can purchase annuities with a joint survivor benefit (lower payout but covers both spouses) and even with a guaranteed payment period to beneficiaries (typically 10-20 years certain).

For a comprehensive analysis of annuities, including detailed discussion of when they do and don’t make sense, see my complete annuities series and my personal analysis where I discuss why I’ve been reluctant despite understanding the benefits—though the dramatically improved rates are making me reconsider.

Bucket #2: RMDs and discretionary spending

The bottom line is that to the extent that you secure enough income to cover your essential expenses through the income floor, you will not need to rely on income from Bucket #2 for that purpose. Whatever you have in Bucket #2 may then be used for discretionary spending (e.g., travel, charitable giving) and future Required Minimum Distributions (RMDs).

RMD ages have changed significantly since the original article:

- Born 1951-1959: RMDs begin at age 73 (was 72)

- Born 1960 or later: RMDs begin at age 75

- Penalty reduced: 25% of shortfall (was 50%), further reduced to 10% if corrected within 2 years

These amounts are predetermined by the IRS based on your age, estimated remaining lifespan, and your portfolio balance. For most, they start in the 3.8-4.0% range at age 73. Everyone with a taxable retirement savings account, regardless of whether it’s a 401(k), 403(b), or IRA, is subject to RMDs. For detailed guidance on managing RMDs, including the strategic use of Qualified Charitable Distributions (QCDs) to reduce taxable RMD amounts, see my article on RMD Withdrawals, QCDs, and Tax Withholding for 2025.

Some may fill Bucket #2 with bonds and dividend stocks, just as they did with the standard bucket strategy. Others may go with CDs or bond ladders. If you have a cash-value or dividend-paying whole life policy, you can use it for this purpose.

With improved yields, bond ladders have become much more practical:

- Individual Treasury bonds: 4-4.5% depending on maturity

- TIPS ladders: 4.5% inflation-adjusted starting withdrawal rate (per Morningstar)

- Investment-grade corporate bonds: 4.5-5.5%

- CDs: 4-5% for 1-3 year maturities

At the very least, you want to cover your RMDs for at least five years or so. The main reason is to ensure that you don’t have to sell the growth assets in Bucket #3 to fund RMDs in the event of a prolonged market downturn.

Bucket #3: Growth assets

Bucket #3 would contain the remainder of your assets. If you used 25-30% for your income floor annuity purchase, and Bucket #2 comprises at least five years of RMD withdrawals (perhaps another 25% of assets), Bucket #3 may include 45-50% or more of your total original savings.

With the modified income floor strategy, depending on how many growth assets you have in Bucket #2, you want to have at least 40-50% of your holdings in Bucket #3 for growth and inflation protection.

Therefore, the investments in this bucket would be a diversified mix of stocks (small, medium, and large-cap, domestic and international, and emerging markets), along with higher-income alternatives like preferred stocks, REITs, and perhaps high-yield bonds for additional diversification.

The income floor approach pairs exceptionally well with variable withdrawal strategies. Since your essential expenses are covered by guaranteed income (Social Security + SPIA + any pension), you can afford to:

- Use guardrails or other flexible strategies with Bucket #3

- Take more equity risk in Bucket #3 (perhaps 50-60% stocks vs. 35-40%)

- Potentially start with higher withdrawal rates (5%+) from Bucket #3

- Reduce withdrawals during downturns without impacting essential living expenses

This combination—income floor for essentials + flexible withdrawals for discretionary spending—is increasingly recognized as the optimal retirement income strategy for many retirees.

Variation #2: Total return approach (simplified two-bucket)

Another strategy is to structure your portfolio with only two buckets—the “cash bucket” and the “investments bucket.” This approach is simpler to manage than the traditional three-bucket or four-bucket strategies.

With this strategy, the cash bucket is more crucial than ever. It would hold at least 3 to 5 years of living expenses in ultra-safe accounts (checking, savings, CDs, or ultra-short-term bonds).

The remainder of the portfolio would be in the “investments bucket.” It would contain a diversified mix of stocks and bonds—typically 40 to 60% stocks for those following safe withdrawal rate guidance.

Bucket #1: Cash Reserve

Like the other approaches, the cash bucket would hold three to five years’ worth of living expenses in cash or cash-like accounts (checking, savings, CDs, money markets, etc.).

You can calculate the amount to put in this bucket by deducting any other retirement income (Social Security, pension, annuity) from your targeted living expenses. For example, if you need $60,000/year before taxes, and Social Security provides $25,000, a 5-year cash bucket would contain $175,000 (($60,000 – $25,000) x 5 years).

With cash and money markets now yielding 4-5%, your cash bucket is earning meaningful returns while maintaining full liquidity and safety. A $175,000 cash bucket now generates $7,000-$8,750 annually in interest—not enough to fully replenish withdrawals, but a significant contribution that wasn’t available in 2020’s near-zero rate environment.

Bucket #2: Diversified Growth Portfolio

You then put the remainder of your retirement funds in a diversified stock and bond portfolio in this bucket—the “growth bucket.” You’ll need to determine what the exact allocation will be. Should it be 100% stocks, a 50/50 allocation to stocks and bonds, or something in between?

Based on current research:

- Morningstar: 20-50% stocks optimal for conservative fixed withdrawal strategies

- Bill Bengen: 47-75% stocks for 4.7% withdrawal rate

- Common practice: 40-60% stocks for balanced approach

The stock/bond portion of such a portfolio may produce some income if it contains dividend-paying stocks or stock funds, but it will take more of a “total return” approach to generating retirement income over the long-term. This means you’ll be selling appreciated assets to fund withdrawals rather than relying primarily on interest and dividends.

It will be more volatile than traditional multi-bucket strategies due to the higher overall allocation to stocks. However, having the 3-5 year cash cushion means you won’t be forced to sell during downturns.

Refilling Bucket #1: Annual Rebalancing

With this approach, you refill your cash bucket once or twice a year through strategic rebalancing. If your target is 50% stocks and 50% bonds, you rebalance the portfolio back to that allocation by selling assets that have appreciated and buying those that have declined.

The result is you are “selling high and buying low,” which is key to long-term success.

The Process:

- Spend from the cash bucket throughout the year for living expenses

- Once or twice annually, rebalance the investment bucket back to target allocation

- Move proceeds from asset sales to replenish the cash bucket

- At age 73/75 (depending on birth year), process RMDs and use those to refill cash

If you follow current safe withdrawal guidance (3.9-5.2% depending on strategy), you will want your overall portfolio to consist of 40% to 60% stocks. (We are taking into account both buckets—cash and investments—to determine our overall asset allocation.)

Your withdrawal rate and this modified bucket strategy work together in some critical ways. As with all bucket strategies, the cash bucket is used for everyday expenses and acts as a buffer against prolonged down markets that negatively impact the investment bucket.

That second aspect—the psychological comfort of not having to sell during market downturns—is of the utmost importance. You want to have enough cash to live on so that you don’t panic and sell during sudden market declines. If five years isn’t enough to give you that comfort level, increase it to 6 or 7. You also need to ensure that your stock allocation is on-target, which is why rebalancing once or twice a year is so necessary.

The two-bucket approach has several benefits:

- Easier to manage: Only two buckets to monitor and rebalance

- Lower cash drag: Reduced from the traditional approach (3-5 years vs. 10 years)

- Higher growth potential: 50-70% of assets in the growth bucket vs. 40-60% in traditional

- Natural rebalancing discipline: Forces systematic selling high/buying low

- Works well with guardrails: Easy to adjust withdrawal amounts based on portfolio performance

This approach pairs well with the guardrails strategy: use the cash bucket for stability, but adjust the amount withdrawn from the investment bucket based on its performance relative to your guardrails.

Choose one if you can

Likely, one of the three “bucket” strategies we have discussed will make sense for you:

- Traditional Bucket Strategy (detailed in my “My Bucket Strategy” article): 10-year reserve, four buckets, moderate complexity, maximum downside protection

- Bucket Strategy with Income Floor: Annuity + Social Security covers essentials, remaining buckets for discretionary spending and growth, optimal for maximizing guaranteed income, particularly attractive with current 8.1% SPIA rates

- Simplified Two-Bucket Approach: 3-5 year cash reserve, diversified growth portfolio, easier to manage, higher growth potential, requires more discipline in rebalancing

For retirees prioritizing psychological comfort and control, the traditional bucket strategy is most effective when a 10-year reserve is maintained, providing maximum peace of mind during extended market downturns. This approach suits those with $500,000- $2 million in savings who value detailed control over asset-sale timing and are comfortable managing moderate complexity, particularly when integrating variable withdrawal strategies. The extended time horizon means you never face pressure to sell depreciated stocks, though you sacrifice some growth potential by maintaining larger cash and bond allocations.

For those with limited savings or high guaranteed-income needs, the income-floor strategy using annuitization is most appropriate, especially for retirees with assets under $500,000 or singles concerned about longevity risk. Current SPIA rates of 8.1% for 73-year-olds are historically attractive, providing significantly higher guaranteed income than any systematic withdrawal strategy while offering simplicity for essential expenses paired with portfolio flexibility for discretionary spending. The trade-off is reduced liquidity and assets passing to insurance companies rather than heirs, but for those prioritizing lifetime income security over legacy, this exchange often proves worthwhile.

For retirees seeking simplicity with reasonable protection, the two-bucket strategy strips away complexity while maintaining core sequence risk protection through 3-5 years of cash and bonds. This streamlined approach works particularly well for larger portfolios ($1 million+) where even a shorter reserve provides ample cushion, suits those comfortable with systematic rebalancing discipline, and allows higher long-term growth potential by keeping more assets in stocks. You accept slightly more volatility than the traditional 10-year bucket approach, but the reduced management burden and increased growth opportunity often justify that modest additional risk for retirees with adequate resources.

No matter which one you choose, be sure to do your homework and seek out professional advice if you need it. Then proceed with confidence that you are stewarding your retirement financial resources well.