This article is part of the Biblically-Informed Framework for Retirement Stewardship (BIFRS) series. It was originally published on August 18, 2021, and updated in April 2026.

When I first wrote this article in 2021, my wife and I had been on Medicare for almost three years. We’d chosen Original Medicare with Medigap Plan F, and I was already confident we’d made the right choice for us.

Now, five years later and nearly nine years into our Medicare journey, that confidence has only strengthened. Our Medigap plan has consistently provided the comprehensive coverage and predictability we wanted.

Our choice was right for us. It’s not necessarily right for everyone. I have friends who are fine with $0-premium Medicare Advantage plans that fit their situations perfectly. The key is understanding the trade-offs and choosing intentionally based on your specific circumstances.

This update includes all 2026 costs, current out-of-pocket maximums, updated enrollment rules, and five additional years of perspective on what these decisions actually mean in practice.

Important decisions

Deciding when to claim your Social Security benefits may be the most important decision you’ll make when you choose to retire. One reason it’s so critical is that, in most cases, it’s irreversible. If you make a mistake, you (and your surviving spouse, if you have one) have to live with it for as long as you live.

The second most critical decision may be how to manage investment risk while generating enough income to live in retirement, especially if you plan to rely heavily on a risk-based investment portfolio to fund a substantial portion of your retirement income.

But a close third is your choice of a Medicare plan.

You may be thinking, “Hey, wait a minute—doesn’t everybody who qualifies get the same Medicare plan?” Well, the answer is yes and no. And selecting the right plan may be more complex and consequential than you think. Fortunately, unlike some Social Security and investing choices, your decision can be reversed, but as we’ll see, not always.

Same but different

We’re approaching the Medicare “open enrollment” period that runs from October 15 to December 7 each year. During this time, you’ll be inundated with TV commercials featuring smiling spokespeople who’ll tell you that you may not be getting everything you’re entitled to from Medicare, and if you call the 1-800 number on the screen, the nice people on the phone will hook you up.

The problem is they’re not actually talking about Medicare, at least not Original Medicare, which is Parts A and B. They’re referring to Part C, Medicare Advantage plans. But this can be confusing because Part C isn’t just an “add on” to Original Medicare that gives you things you’re entitled to that you weren’t getting before. (I’ll explain more later.)

Yes, Medicare is Medicare—it has Parts (A, B, C, and D). How the government defines these plans affects all Medicare benefit recipients, regardless of which plan they choose. But there’s much more to it than just the A-B-Cs.

You could opt for Original Medicare, which covers Parts A and B. It’s important to understand the basics of Medicare Parts A and B; you can read “Medicare Health Insurance Options” for a comprehensive overview. Also, the government’s Medicare website is an excellent source of information.

But if you only go with Parts A and B, you’ll have significant exposure to the expenses they don’t cover—particularly the 20% coinsurance after you meet your deductible, which has no annual cap. That’s why choosing the right Medicare plan is so important.

My wife and I went on Medicare almost nine years ago, so I know from experience how confusing it can be. For the first time in about 40 years, we had to transition from the relative safety and security of an employer-sponsored group health insurance plan to a government-sponsored and administered plan.

Like other 60-somethings, we had to make our own decisions about Part B, Part C (Advantage Plans), Supplemental Plans (Medigap), Part D (prescriptions), vision, dental, and more. And like almost everyone else, we had to choose between the two main paths: Original Medicare (Parts A and B) with a “Medigap” supplemental plan along with vision and dental plans, or a Medicare Advantage plan (Part C) to get the coverage we needed to prevent significant out-of-pocket expenditures for the things Parts A and B don’t cover.

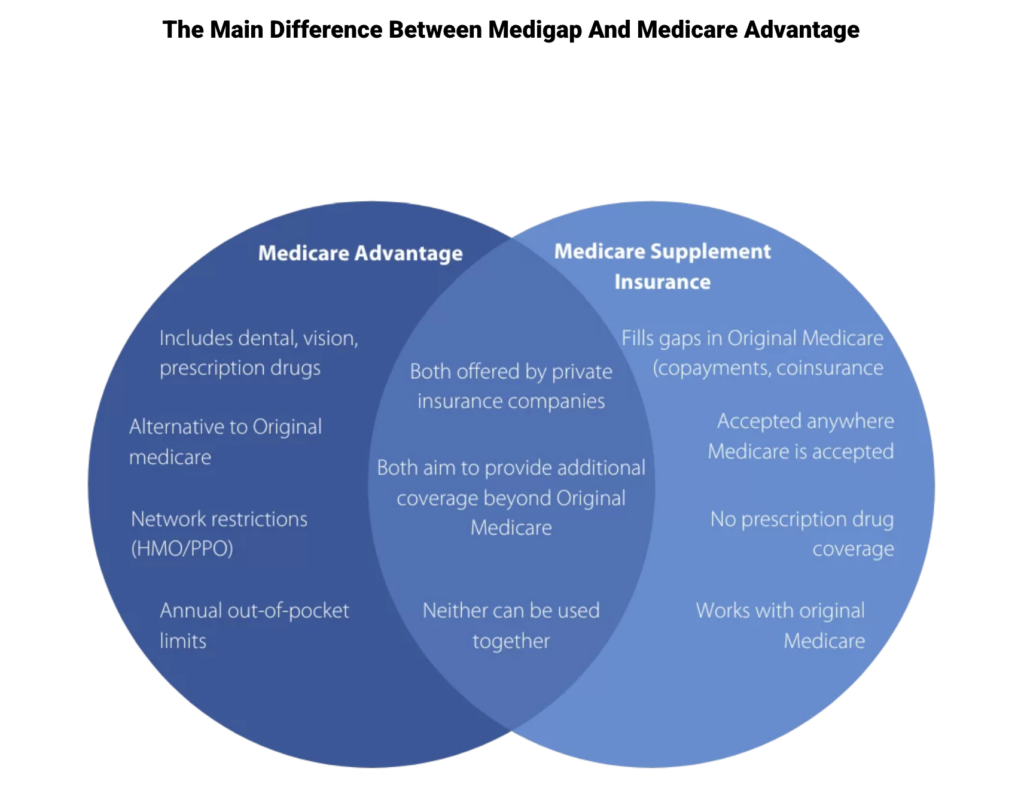

Here’s a graphical comparison of the two types of plans, with additional details below it.

Original Medicare + Medigap:

- Parts A and B coverage

- Add Medigap supplement (Plans A-N)

- Add a separate Part D prescription plan

- Add separate vision/dental if desired

- See any doctor accepting Medicare nationwide

- Predictable costs, minimal paperwork

- Higher monthly premiums

Medicare Advantage (Part C):

- Replaces Parts A and B (but you still pay Part B premium to the government)

- Usually includes Part D prescriptions

- Often includes vision, dental, and hearing

- May include fitness, meal delivery, and transportation

- Network restrictions apply

- Lower or $0 premiums

- Out-of-pocket maximums apply ($9,250 in 2026)

IMPORTANT: Note that neither Original Medicare nor either of the above-described plans covers long-term care (nursing home, assisted living, memory care). If you want insurance for that, you’ll have to purchase long-term care insurance. If not, you’ll have to pay it out-of-pocket. If you can’t afford it, you may have to go the Medicaid route.

Supplemental Plans (“Medigap” Insurance)

A Medigap plan is supplemental to Medicare Parts A and B. Medicare typically pays 80% of covered charges (after you meet the Part B deductible of $283 in 2026), and a Medigap plan typically pays “the rest”—the 20% coinsurance, deductibles, and other gaps. How much of “the rest” depends on which type of Medigap plan you select.

Neither Medicare nor Medigap plans cover prescriptions, vision, or dental, like most employer plans do. So if you choose a Medigap plan, you’ll also need to purchase a separate Part D prescription drug plan and potentially separate vision and dental supplements.

2026 Medigap Plan Costs:

Medigap plans cost approximately $125-$260 per person per month, depending on your age, location, tobacco use, insurance carrier, and which Medigap plan you select. Plans are standardized (A through N) and differ primarily in what coinsurance, copays, and deductibles they cover.

The Most Popular Medigap Plans in 2026:

Plan G (most popular for new enrollees):

- Covers nearly everything except the Part B deductible ($283/year)

- Typical cost: $125-$260/month, depending on age and location

- Best value for most people

Plan F (no longer available to new enrollees):

- Most comprehensive—covers everything, including the Part B deductible

- Only available if you became Medicare-eligible before January 1, 2020

- What my wife and I have (grandfathered in)

Plan N (growing in popularity):

- Lower premiums than Plan G

- Small copays ($20 office visit, $50 ER visit)

- Good for healthy people who don’t see doctors frequently

Important: Medigap “plans” (A through N) are different from Medicare “parts” (A, B, C, and D). Don’t confuse them.

(For complete Medigap plan details and 2026 costs, see Medicare Health Insurance Options.)

Medicare Advantage Plans

The best way to think about Advantage plans is to think of them as a “bundled” product that includes Parts A, B, and usually D (prescriptions), often with vision and dental coverage as well.

Private insurance carriers such as Blue Cross, Humana, United Healthcare, Cigna, and others offer these plans. The government specifies that they must provide at least what Original Medicare (Parts A and B) offers, but they usually add more benefits to make their products attractive (free gym memberships, meal delivery, transportation, over-the-counter allowances, etc.).

The Most Important Things to Know About Advantage Plans:

1. They’re managed-care plans with networks. You’ll have in-network and out-of-network providers. Your costs will be lower in-network, but you may not be able to see any doctor you want.

2. They have out-of-pocket maximums. In 2026, the maximum out-of-pocket limit for in-network services is $9,250 per person (down slightly from $9,350 in 2025). This is the most you’d pay for covered services in a calendar year. Some plans set the maximum lower, but they can’t go higher than the federal cap.

3. Many have $0 premiums. Unlike Medigap plans that cost $125-$260/month, many Medicare Advantage plans claim to be “free”—there are zero premium costs per month beyond your Part B premium to the government.

4. You still pay the government for Part B. Even though your Advantage plan is “free,” you still pay the standard Part B premium ($202.90/month in 2026, or higher if IRMAA applies). The government collects this money and transfers it (plus additional funds) to your insurance carrier to manage your plan.

You’re probably wondering, “What’s the catch?” Well, there really isn’t a hidden catch. They aren’t deceiving you. However, there are trade-offs when you choose one plan over the other, and that’s the main thing you need to understand.

If you’re like me, you’d want a Medigap plan that costs zero like Medicare Advantage, one that includes prescriptions, vision, dental, and the other “perks” you hear about on TV. Sorry, that’s not going to happen; there’s no such thing. (The closest is Medicaid, which varies from state to state and may include vision and dental benefits for qualifying low-income seniors.)

Trade-offs: the whole truth

You may have heard those Medicare commercials on TV. The next time one comes on, listen for the phrase “things you’re entitled to” (which, as I’ve written before, is a little misleading) and the word “free” (which is true but doesn’t tell the whole story). You’ll hear both repeated several times.

If you choose Medigap, you aren’t going to get all the things that the friendly announcer on TV talks about in that commercial: the free dental, transportation, meal delivery, vitamins, gym memberships, etc. Those things aren’t covered by Medicare Parts A and B, and Medigap policies follow Original Medicare—they only fill in the gaps that Original Medicare leaves, nothing more.

The commercials are for Medicare Advantage plans. And if you pick Medicare Advantage, there’s a trade-off. You may not be able to go to any doctor you want. You may need prior authorization for certain procedures. Your specialists must be in-network, or you’ll pay significantly more.

On the other hand, you may pay little or no premium (beyond Part B,) and you’ll get those extra benefits like dental, vision, gym memberships, and meal delivery.

A realistic scenario:

If you (and your spouse) are relatively healthy, take a prescription or two, and typically only visit the doctor once or twice a year for check-ups, you’ll probably gravitate toward a Medicare Advantage plan. After all, it may be free. Why pay more than free if you don’t anticipate a lot of additional medical expenses? Plus, you can go to the gym for free and get your teeth cleaned twice a year for free as well.

Meanwhile, your friends with Medigap (if they are a couple) are probably paying $ 500–$600+ per month for combined Medigap, vision, and dental insurance. That’s in addition to the cost of Medicare Part B, which is $405.80/month for a couple at the standard rate in 2026 ($202.90 × 2), but it may be significantly higher based on your Modified Adjusted Gross Income (MAGI) due to IRMAA surcharges.

Our personal experience

I have a Medigap plan (Plan F), vision, and dental. My wife and I were a lot like the couple I described above, with only occasional doctor visits and a few prescriptions. But then my wife had a ruptured appendix in Fall 2020 (which required hospitalization but no surgery) and has been receiving treatment for a torn rotator cuff that ultimately required surgery.

Since first enrolling, our Medigap Plan F has covered everything beyond the Part B deductible in every case. We’ve never received a surprise bill. We’ve never had to check if a doctor was in-network. We’ve never needed prior authorization.

With my Medigap plan, I haven’t paid anything out of pocket beyond premiums for any of these medical situations. If we had been on a Medicare Advantage plan, we almost certainly would have paid the out-of-pocket maximum each year for the years with significant medical expenses, which would have been $9,250 per person in 2026 (assuming all doctors and services were in-network).

Changing plans: the unexpected “trap”

People are turning 65 every day, and they need to start thinking about Medicare coverage two or three months before their 65th birthday. Once you get Parts A and B set up with Medicare, you then need to decide which of the two coverage options you prefer—Medigap or Medicare Advantage.

But the situation is different for those already enrolled in a plan, and this is where many people get trapped.

Suppose you have a Medicare Advantage Plan but would like to switch to Original Medicare with a Medigap policy to get better coverage and more options for a serious diagnosed condition. You may run into a significant problem: You may not qualify for a Medigap plan if you’ve been diagnosed with a serious condition.

Insurance companies can consider pre-existing conditions and can deny coverage or charge significantly higher premiums. If you’ve been diagnosed with conditions such as cancer, COPD, diabetes, heart disease, stroke, ALS, or other serious health issues, you may not be able to get Medigap coverage at all.

Your only options would be to either:

- Stay on Original Medicare (Parts A and B only) and pay the 20% coinsurance out-of-pocket with no cap (not a good option)

- Re-enroll in the same or a different Medicare Advantage Plan in your area

- Pay dramatically higher premiums for Medigap if any company will accept you

You may run into the same problem if you want to switch from one carrier’s Medigap plan to a different carrier’s plan. They can consider pre-existing conditions and can deny coverage or charge a higher premium for it. (A few states—including California, Connecticut, Maine, Massachusetts, Missouri, Nevada, New York, and Oregon—have special rules that allow their residents to switch Medigap plans regardless of preexisting conditions, either year-round or during certain times.)

You can, however, change Medigap plans from the same carrier (such as going from Plan C to Plan G). You’ll just have to pay the higher premium for the more comprehensive plan.

So don’t assume that you can switch plans at will.

The critical window

When you enroll in Medicare Part B, you have a special six-month Medigap Open Enrollment Period when you can’t be denied a Medigap plan due to a pre-existing condition. This is your “personal open enrollment window,” and it’s guaranteed issue—no medical questions asked, no health conditions considered, no denials possible.

But this only happens when you’re a new Medicare Part B enrollee and are age 65 or older. (Remember, you must enroll in Part A when you turn 65, but many people remain on their employer plan and don’t enroll in Part B until later.)

This is why I emphasize regret minimization: A Medicare plan may seem right for now, but what if your situation changes? What if you develop a serious condition? If you start with Medicare Advantage and later want to switch to Medigap, you may not be able to—or you may face prohibitively expensive premiums.

Choosing a plan: decision framework

I want it to be clear that I am not suggesting that Medicare Advantage Plans are bad and that no one should enroll in one. I’m saying that you need to be a wise, educated consumer so that you understand the pros and cons of the different plans and choose accordingly.

Choose Original Medicare + Medigap if you:

- Value freedom to see any doctor accepting Medicare nationwide

- Travel frequently or split time between multiple locations

- Have chronic conditions or anticipate needing specialists

- Want predictable costs and minimal paperwork

- Can afford higher monthly premiums ($500-600+/month for a couple)

- Want to avoid network restrictions and prior authorization requirements

- Prefer comprehensive coverage with minimal out-of-pocket costs

Choose Medicare Advantage if you:

- Want lower or $0 monthly premiums (beyond Part B)

- Are generally healthy with minimal medical needs

- Don’t travel much and are comfortable with network restrictions

- Want dental, vision, hearing, and fitness benefits included

- Are comfortable with prior authorization for certain procedures

- Can handle potential out-of-pocket costs up to $9,250/year if needed

- Prefer an “all-in-one” plan that bundles everything together

Neither choice is inherently wrong. The key is choosing intentionally based on your specific situation and risk tolerance.

Important things to know about advantage plans

Here are some of the other most important things to know about Advantage plans:

1. They vary by location. Medicare Advantage Plans differ significantly from state to state and even county to county. Because commercial carriers provide them, they’re regulated by individual state insurance commissions. What’s available in Florida may be completely different from what’s available in Oregon.

2. They have networks. When you receive a service, you’ll be in or out of the network. Your costs will be dramatically lower in-network. Make sure you’re okay with being told which doctors you can and cannot use, and verify that your current doctors are in the network before enrolling.

3. You may pay little or no premium (beyond Part B), but you will have copays and coinsurance fees. As noted previously, these can add up to the out-of-pocket maximum ($9,250 per person per year in 2026). For a couple with significant medical needs, that could mean $18,500 in a single year.

4. They must cover all services that Original Medicare covers. However, a plan can choose not to cover the costs of services that aren’t deemed medically necessary under Medicare guidelines. Advantage plans offer coverage for things not covered by Original Medicare, such as vision, hearing, dental, and wellness programs (like gym memberships).

5. Your plan may require prior authorization. You’ll need to carefully read your plan’s coverage contract to determine which services, or how many, require prior approval. This can delay care and create administrative hassles.

6. Out-of-network costs can be very high. If you see an out-of-network doctor or receive services at an out-of-network facility, you may pay significantly more or even the full cost yourself. The $9,250 maximum only applies to in-network services.

Costs and trade-offs matter

I said earlier that what I really want is a no-cost Medigap plan. Maybe you would too, but as you now know, there is no such thing (although Medicaid comes close for qualifying low-income individuals). The thing about Medigap policies is that many people can’t afford the additional premiums (in addition to Part B). Plus, they also need a Part D prescription drug plan. And they may also want dental and vision supplements, which would add more costs.

Typical Monthly Costs for a Couple (2026):

Original Medicare + Medigap:

- Part B premiums: $405.80/month ($202.90 × 2)

- Medigap Plan G: $350-520/month ($175-260 × 2)

- Part D prescriptions: $70-100/month ($35-50 × 2)

- Vision/dental: $80-160/month

- Total: $905-1,265/month or $10,860-15,180/year

Medicare Advantage:

- Part B premiums: $405.80/month (same as above)

- Advantage plan premium: $0-80/month (many are $0)

- Copays and coinsurance: Variable (could be $0-9,250/person/year)

- Total: $405-565/month guaranteed, plus potential out-of-pocket costs

Now we’re talking about potentially several hundred dollars difference per month, so a zero-premium “all in one” Advantage plan may be much more attractive—especially if you’re healthy. But remember, you’ll make some sacrifices if you go that route: network restrictions, prior authorizations, potential high out-of-pocket costs if you get seriously ill, and difficulty switching back to Medigap if your health changes.

The bottom line: Medicare Advantage plans are good for the government (risk transfers to the private insurance carrier). They’re also good for the carriers (their government payments are basically guaranteed). One may also be good for you, but as we’ve seen, they’re not everything they’re made out to be in TV commercials.

A stewardship perspective

That said, I view Medicare and the various Medicare plans as part of God’s gracious provision for those who need healthcare in retirement, which is pretty much all of us. No plan is perfect. There are always trade-offs, but what you give up matters.

So if you’re Medicare eligible, before even thinking about one plan or another, think about:

- What kinds of coverage do you need

- What you’re willing to pay each month

- Whether you’re willing (and able) to pay high out-of-pocket costs for some services

- Whether you value provider flexibility or are comfortable with network restrictions

- How your health might change over the next 10-20 years

Then look at your plan options carefully using Medicare’s Plan Compare tool, make sure you understand all the terms and conditions and associated costs (get advice and counsel if you need it), and come to grips with what you are willing to sacrifice in one type of plan for something you really want in another.

And before you decide, visualize yourself 5, 10, or 20 years out and consider whether your decision may be one you might regret should your health significantly deteriorate, or you develop a serious condition requiring highly specialized care.

Plan and choose wisely so that when you need care (and you will), you can receive it without creating a financial crisis for yourself or your family.

“The prudent see danger and take refuge, but the simple keep going and pay the penalty.” (Proverbs 27:12, ESV)

A final reflection

After nearly nine years on Medicare with our Medigap Plan F, here’s what I know for certain: We made the right choice for us. The higher monthly premiums have been more than offset by the peace of mind, comprehensive coverage, and complete provider flexibility we’ve enjoyed.

But I also know friends who are equally happy with their $0-premium Medicare Advantage plans. They’re healthy, don’t travel much, like their network doctors, and save thousands of dollars annually on premiums.

The key is this: Choose intentionally. Understand the trade-offs. Don’t just pick what your neighbor has or what the TV commercial promises. Think through your specific situation, your health trajectory, your values (do you prioritize flexibility or cost savings?), and make a decision you can live with for the long term.

And do it during that six-month Medigap Open Enrollment window when you first enroll in Part B. That’s your one guaranteed opportunity to choose Medigap without any health questions. Don’t waste it.