It took me a while to publish this last article (at least I think it’s the last one) in this series on bonds, bond funds, bond ladders, and Treasury Inflation-Protected Securities (TIPS)—whew!

As I worked through these topics and TIPS ladders, in particular, the path seemed clear. But then I had some concerns—not about TIPS ladders per se’ (I think they’re a great idea and make sense for a lot of people), but whether building one really makes sense for me.

The question I’ve been wrestling with is this: With higher current yields and the prospect of higher-than-normal inflation, should you or I construct a bond ladder or, more specifically, a TIPS ladder for ‘safer’ retirement income, or will the bond or TIPS fund I already own do the job just fine?

Stepping on the ladder

Like many people, the current much higher than usual interest rates attracted me to building a bond ladder. And for a good reason: to “lock in” current high-interest rates that probably won’t stay this high for very long (but then, who knows?).

Once I started thinking about a ladder, as you’ll recall from previous articles, I soon shifted my focus to individual TIPS bonds because they are showing better returns since over a decade ago, but as I explained in the last article, a long-term TIPS ladder doesn’t appeal to me.

(That doesn’t mean it’s not right for you. You may want to consult with a financial advisor if you’d like to explore that option further; there’s a great Morningstar article on how to build a long-term TIPS ladder.)

I now think an intermediate-term TIPS ladder might be a better option if I did build one. But I keep coming back to the same question: is an excellent short-term TIPS fund, like STIP, which I already own, good enough that I don’t have to go through the pain of building the ladder, and how can I know?

With either approach, I’ll get inflation protection, but if inflation is average, I’ll get Treasury bond returns. If inflation is higher than expected, I’ll do better than nominal Treasuries.

The big difference between those two options is interest rate risk. The TIPS ladder may make better sense if interest rates are higher than expected. But if they rise and then fall, which tends to cause share prices to “normalize,” but if I hold on to my STIP fund through all those ups and downs, I may end up okay.

In fact, over time, bond fund returns can rise even if interest rates rise. That’s because bond funds contain bonds with defined maturities. And their value tends to move back closer to ”par value” (original face value) if held to maturity. That’s why holding bond funds with an average duration that matches your needs for income makes good sense.

So what should I do?

That’s the question I’ve been asking myself. I am reluctant to make significant changes to my portfolio. I have a basic strategy that has shared me reasonably well so far, with a tweak here and there.

I’m not dogmatic about never changing anything. Changing economic conditions prompted my shift into short-term funds and moving cash into government MMA and short-term TIPS (STIP) about a year ago. And I’ve made other tweaks, such as adding a real estate index fund.

Still, I could shift some of my savings into a TIPS ladder by purchasing individual TiPS in the secondary market with my online brokerage account. But all I’ve learned about that suggests that it can be complex and tedious.

So, I decided to see at least what that might conceptually look like by incorporating it into my bucket strategy.

Ladders and buckets

All we need now is a firetruck!

I can see how I might integrate a TIPS ladder into my bucket strategy.

First, looking at the short term, I have a couple of years of expenses in cash (I currently have them in a Fidelity government money market fund). I could start the ladder a couple of years out, but it may make just as much sense to keep that money in my STIPs fund (a 0-to-5-year TIPS fund).

I’m sure there’s a good way to analyze how one would perform versus the other over the short term, but I don’t think it’s worth spending time and energy on it.

I also have some money in a short-term bond fund, which holds Treasury and corporate bonds, so I can easily cover the first few years of spending before my TIPS ladder kicks in. It could partially replace some of my intermediate-term bond fund investments.

Remember, the concern here is inflation risk—not necessarily the current year or even the next few, but persistently high inflation 5, 10, or 15 years out. And since my portfolio isn’t stock-fund-heavy, I can’t rely entirely on stocks to “carry my inflation water.”

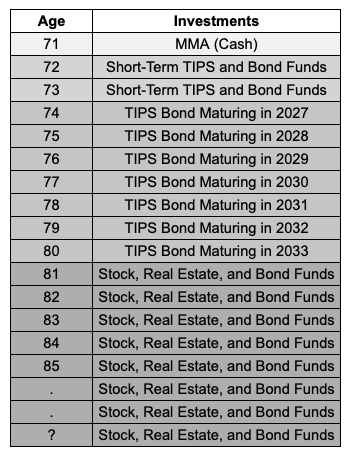

If I use cash (in an MMA) and short-term TIPS and other bond funds for the first few years of the ladder and then build a seven-year TIPS ladder, I’d have ten years of reasonably sure retirement income. I’d then use stock, real estate, and intermediate to long-term bond funds for income needs beyond age 80.

Medium-Term TIPS Ladder

Based on current interest rates (the “inverted yield curve” and all that), there is a sweet spot in the intermediate range of bonds with maturities longer than three years but less than 7 to 10 years.

History (which may or may not repeat) has shown that stocks, on the other hand, rarely lose money if you hold them for ten years or more.

As my ladder rolls along, I must decide what to do with each TIPS bond as it matures—spend it, reinvest it, or some other purpose.

As I have discussed in recent articles, a significant benefit of TIPS bond ladders is that they are relatively free of interest rate risk if we hold individual bonds to maturity. If rates rise, I won’t lose money on the TIPS ladders. If I stay in my bond funds, the share prices will decline, but yields will increase.

Plus, if I have to sell bonds or bond fund shares, I may do so at a loss. I don’t intend to do so, but as we know, life happens.

Situation, situation, situation

In buying real estate, some say it’s “location, location, location.” When it comes to investment decisions, it’s your “situation, situation, situation,” and how different considerations apply to yours.

In this case, it seems to come down to three primary considerations. The most important one for you will depend on your situation.

1 – Where is the money you want to use your TIPS ladder coming from?

2 – When do you need the money (not just income from it, but the investment capital itself to spend in retirement)?

3 – What risk are you trying to avoid—rising interest rates, inflation, or both (but to be clear—no investment carries zero risk; if it did, it probably wouldn’t be called an investment)?

Let’s look at a few scenarios and what an optional solution might be in light of the above considerations.

Scenario #1:

The money is from “safe” (cash, CD, etc.) investment that you want to earn higher returns on; you’ll need to spend the money at a designated time in the future (e.g., income, planned expense, etc.); and, you want returns at least equal to inflation but also concerned about interest rate risk (rates may go down in the near term but are likely to rise again rapidly in future years).

Optional solution: TIPS Ladder

Scenario #2:

You have the money in diversified bond funds (short and perhaps intermediate-term maturity), which lost money last year. While you won’t need the money to spend, you want to maximize income for spending in retirement. You’re concerned about interest rate and inflation risk. (This closely resembles my situation.)

Optional solution: duration-appropriate TIPS and bond funds

Scenario #3:

Some combination of the above two. For example, the money is from a short-term MMA but you don’t need to spend it at a particular time, and you’re concerned about inflation and interest rate risk.

Either a TIPS ladder or bond funds may be an acceptable solution. If this were me, I’d probably lean toward a TIPS ladder, at least for a significant portion (I could mix a ladder and fund).

Ladders of funds

To take things a little further, if I were less concerned about inflation and more about interest rate risk, I might consider an investment you may not have heard of: specific maturity date ETFs.

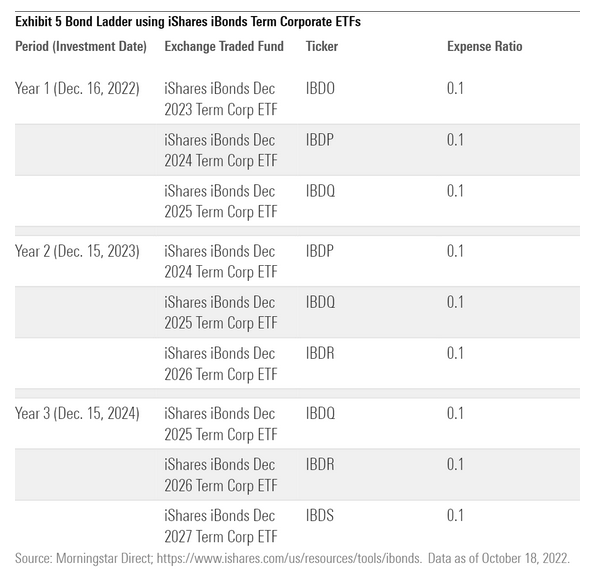

Here’s a description from an excellent article from Morningstar about using these products to build a bond ladder instead of purchasing individual bonds:

Unlike a typical bond fund that holds bonds with a range of maturities and buys new ones when the old ones mature, defined-maturity ETFs try to mimic the behavior of an individual bond. Each ETF sticks to a predefined maturity date by only buying bonds from a purpose-built index that matures in the year the ETF terminates.

The article illustrates what a 3-year bond ladder would look like using a mix of iShares iBond ETFs:

Another major ETF provider that offers a similar product is Invesco (Bullet Shares). However, only iShares offers treasury bond funds, and Invesco exclusively includes emerging markets debt funds in their suite of products.

If interest rates rise, and I hold the EFTs until they liquidate (usually at the end of the year when all bonds mature), I’d get back whatever I paid for them (not their original face value), plus I’d have the interest income along the way. Not a bad deal at all–exactly how an individual bond ladder would have worked.

Meanwhile, my bond funds would have lost value, but their yields would have increased.

There’s a lot to like about these funds. And if you or I were to choose them as part of a ”bucket strateg,y” what might that look like?

I would partly depend on which of the above three scenarios you’re in, but let’s take my situation. I’d replace bond ETFs with duration targets with bond ETFs with specific maturity dates. The advantage, as discussed, is that I’d lock in the interest rate and interest rate protection (if I hold the laddered ETFs to their maturity).

Because I’m not too fond of long bonds, and most of my current bond funds’ target durations are in the 2 to 7-year range, laddered ETFs would fit in bucket #2 of my bucket strategy. They would provide predictable cash flows with capital to redeploy or spend at the end of each year. If I didn’t have to sell before then, I wouldn’t lose any “principal.”

Stepping on another ladder

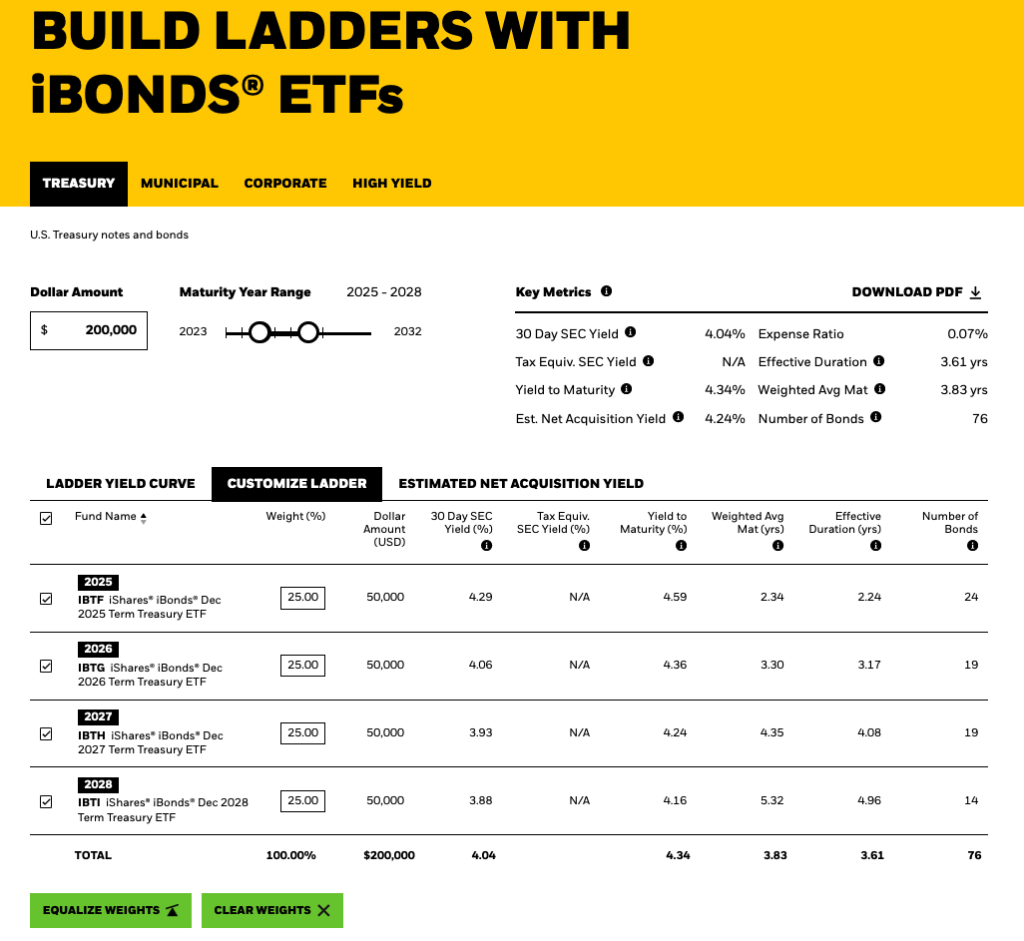

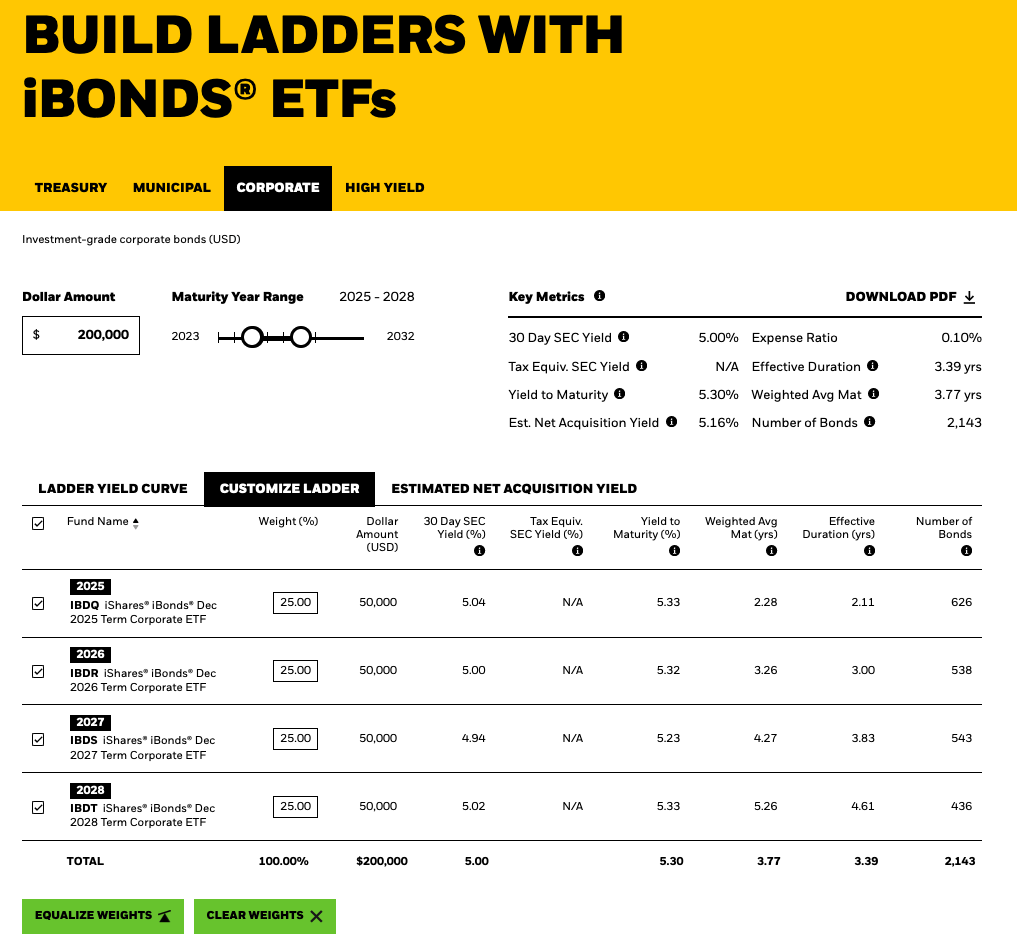

If I were to build such a ladder, I’d probably use iShares iBond (available at Fidelity with no commissions). I’d also have a mix of treasury and corporate bonds but stay away from high-yield (higher risk) bonds.

Here’s what a hypothetical $400,000 ladder might look like, split equals between the two. First, the treasury bonds:

Next, the corporates:

You can read the charts for yourself, but what stands out to me is that the combined “yield to maturity” for this bond portfolio from now until the end of 2027 is 4.77% with no loss of principal IF you hold each fund to maturity.

Worth considering, I think so. Just keep in mind that the corporate funds carry some default risk, but based on their composition, it’s probably in the 2 to 3 percent range.

But guess what? My short-term bond index fund (BSV) has a 30-day yield of 4.51% and fees of .04% (less than the iShares shares). My iShare corporate bond fund (USIG) has a 30-day yield of 5.32% and expenses of .04%. So both are (currently) performing as well as the ETF ladders.

The key difference, as said, is the effect of rising interest rates on the different funds if they are held until the end of 2028.

What am I going to do? Well, for now, nothing. But I have to confess–TIPS are very attractive now, and a bond ladder of specific maturity ETFs looks interesting too. But I need to figure out if they would really be that much better than holding on to my bond funds. At this point, I don’t think so IF I don’t have to sell bond fund shares at a loss after they have gotten hammered by higher interest rates in the years ahead.

Perhaps having some protection from that is a good idea. I’ll let you know what I decide.

A closing thought: Learn, pray, seek wise counsel, and then, “rust in the Lord with all your heart, and do not lean on your own understanding. In all your ways acknowledge him, and he will make straight your paths (Prov. 3:5–6, ESV).